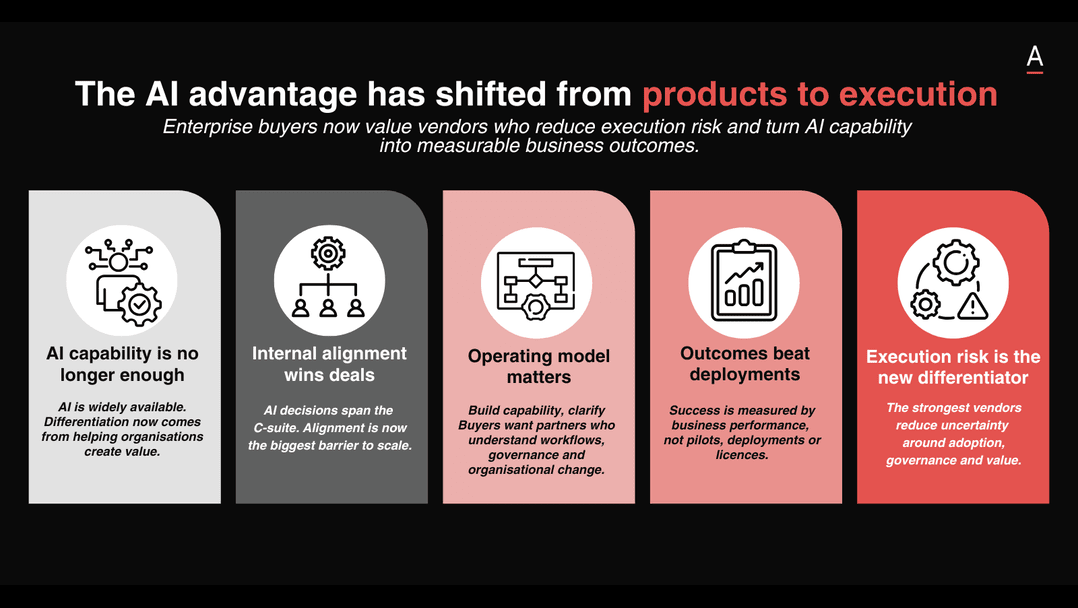

Enterprise buyers have moved beyond AI products. Has your GTM strategy?

Vendors now need to lower the execution risk around AI-led change and help buyers turn capability into measurable organisational value.

Published Jul 15, 2026 in

Go-To-Market

Contributors

Justina Uy

Published Jul 15, 2026 in

Go-To-Market

Contributors

Justina Uy

The AI sales conversation is starting in the wrong place.

Vendors often lead with the platform, the copilot, the agent, the roadmap or the implementation pathway.

Inside the buyer’s organisation, the harder questions sit upstream.

Who owns the change? Which workflows need to be redesigned? What governance will hold when AI moves from pilot to production?

How will the CFO, COO, CHRO, risk and technology leaders agree on value?

Digital & AI Edge last June 2026 positioned AI buying as an organisational change conversation, with software selection only one part of the decision.

Leaders were trying to understand why similar technologies produce different outcomes, why pilots fail to change work, and why organisational readiness now determines whether AI investment becomes value or another layer of complexity.

Many are still selling AI as a technology decision while buyers are trying to work out whether their organisation can absorb the change.

A stronger GTM strategy starts inside that uncertainty.

It helps the buyer understand what must change around the technology before value can scale.

In this article, we’ll examine:

- AI capability’s declining power as a differentiator

- Internal alignment as the buyer’s hardest execution problem

- Operating model fluency as a new measure of vendor relevance

- The shift from deployment proof to changed business performance

AI capability is losing power as a differentiator

Most buyers already have access to powerful AI through GPT, Claude, Gemini, Copilot, agentic platforms and AI-enabled enterprise software.

They can work with global providers, local specialists and consulting partners, and they can launch pilots across almost every function.

For vendors, demand is high, but differentiation is narrowing.

Capability is easier to compare, replicate and bundle into existing enterprise platforms.

The harder buyer question is whether that capability can translate into measurable organisational change.

Gabby Fredkin, Head of Analytics & Insights at ADAPT, showed the scale of the execution gap at Digital & AI Edge.

While 77% of leaders were actively investing in AI agents, only 7% of organisations reported meaningful change to the way work is done.

Investment is moving quickly, but impact is uneven because organisations differ in how well they absorb technology-led change.

Similar AI tools produce different outcomes because the surrounding system differs: leadership, governance, workflows, data foundations, decision rights, funding discipline and workforce readiness.

David Walker, former Group Chief Technology Officer at Westpac and DBS and Chair of the AI Council at UNSW, reinforced that point.

He revealed that 70% of the barriers to scaling AI are organisational, including finance systems, governance models, leadership, process change and adoption, while only a much smaller share relates to AI technology itself.

Transformation credibility is becoming a commercial requirement.

Buyers increasingly need to know whether a vendor understands the conditions that shape value: architecture, security and integration, but also governance, adoption, data, workflow redesign and executive ownership.

DBS shows what this can look like in practice.

The bank scaled AI after building cloud-enabled architecture, digital channels, a common data lake and a platform operating model where business and technology leaders co-created products and shared accountability.

AI had stronger conditions to scale because the organisation had already invested in data, experimentation and customer relevance.

The opportunity is to help them assess whether AI can work inside their organisation, with their governance, workforce, workflows, data and executive politics.

Discovery can start with the organisational change required for value, then work back to where the product fits.

The buyer’s hardest problem is internal alignment

AI buying is moving higher because its consequences now cut across the enterprise.

CIOs, CTOs and CDOs remain central, but the decision increasingly involves the CEO, COO, CFO, CHRO, risk, legal, operations and customer leaders.

Once AI changes how work is designed, decisions are made, risk is governed and value is measured, the buying committee changes with it.

Many vendor motions still treat AI as an implementation sequence: install, integrate, configure, automate, scale.

Buyers are often wrestling with a different question: what should the work become now that intelligence can sit inside more of the process?

Dawid Naude, CEO at Pathfindr, argued that AI behaves more like a universal capability than a conventional enterprise system.

Organisations get stuck when AI is delegated too quickly to the CIO, CTO or a project office, because business leaders need to use it directly and understand how it changes strategy, prototyping and decision-making.

That creates a credibility test before procurement begins.

A provider selling AI into executive buyers needs fluency in the business change around the tool: how decision-making changes, how teams redesign work, how governance keeps pace and how value is measured once the technology enters live workflows.

Dawid’s challenge to buyers was practical: ask vendors how they prepared for the meeting.

If a vendor claims AI expertise but cannot show how it used AI to understand the buyer’s organisation, industry, problems and priorities, the sales interaction weakens the claim.

Generic account research, thin personalisation and product-first decks are now commercial liabilities.

They suggest the vendor is using AI as a message, not as an operating capability.

Mark Cameron, ADAPT Executive Advisor and CEO & Director at Alyve, identified leadership approach as the clearest pattern separating organisations getting significant return from those getting little value.

The top performers connect AI to the organisation’s mission and ask what more the organisation can do that it could not do before.

He also described the executive cohesion problem.

Boards and leadership teams may agree that AI matters, while finance, risk, revenue, product, workforce, customer and technology leaders pull towards different concerns.

Everyone supports AI in principle, but the organisation stalls because the leadership system is not aligned on the change.

Commercial value starts earlier in the conversation.

A stronger discussion helps the buyer map executive alignment, governance exposure, workflow assumptions and success measures before the decision narrows to technology.

A weaker discussion leaves the buyer to translate product capability into an internal case for change.

Vendor relevance now depends on operating model fluency

Buyers are trying to understand how work should change because AI exists.

Many vendor conversations still centre on implementation: what can be installed, integrated, configured, automated or scaled.

The more valuable conversation starts with work design, decision flow and ownership.

Bhaskar Katta, General Manager at Westpac, described the operational discipline behind AI value from a practitioner’s view.

Westpac’s journey moved through automation, process and task mining, intelligent document processing and knowledge support before agentic capability entered the picture.

According to him, there is no AI without process intelligence.

A buyer with poor process visibility does not need a faster automation pitch.

They need help understanding where work actually happens, where handoffs slow execution, where value leaks, and where AI would improve the system rather than accelerate the wrong activity.

Jen French, General Manager AI Acceleration at CommBank, described the complementary discipline.

CBA works back from the desired outcome, using design thinking and systems thinking to reimagine the process before deciding where AI belongs.

For vendors, this raises the standard for discovery.

The question is not simply which AI use case the buyer wants to pursue.

The better question is what organisational change has to happen before the technology delivers value.

That moves the conversation towards future operating models, decision flows, commercial priorities and cross-functional ownership.

It also forces a more honest view of where the buyer is ready, where the organisation is exposed, and where a technology-led project would stall.

Mark Pesce, ADAPT Executive Advisor and Co-Founder at Wisely AI, adds another layer to the operating model discussion.

He described AI as a repricing of cognition, where work that once depended on expensive human thinking can now be performed, supported or accelerated by agents at a different cost structure.

Organisations designed around old cognition costs may find their processes and business models no longer fit the new economics.

A vendor that can discuss this credibly enters a different buying conversation.

The discussion shifts from product comparison to how cost structures, value chains, roles and workflows change when intelligence can be embedded across more of the organisation.

Product capability can get a vendor into the category. Operating model fluency keeps the vendor relevant to the executive agenda.

Proof has moved from deployment to changed performance

The AI market is moving from experimentation to accountability.

Buyers are becoming less tolerant of proofs of concept, innovation theatre and isolated pilots that do not alter performance.

Time saved, licences deployed, pilots completed and users onboarded may show activity, but they do not prove that the organisation has improved.

Dan Chesterman, CIO at Teachers Mutual Bank Limited, argued that organisations need to baseline performance before applying AI, otherwise they risk measuring the launch of a tool rather than whether customer experience, process performance or business outcomes improved.

Loose ROI language is becoming easier to challenge. A productivity claim is weak without a before-state. A pilot story is weak if it cannot explain what changed in the work. A deployment metric is weak if it does not connect to decision quality, customer experience, risk outcomes, cost-to-serve or revenue performance.

Andrew Brain, Director, Data AI and Growth at Southern Cross Media Group, made the commercial discipline clear in a disrupted media environment.

His teams are expected to know the commercial value of their work, challenge requests that do not drive outcomes and focus on the priorities that matter.

In a market where traditional revenue models are being pressured by digital platforms, AI creates value when it helps the business understand audience, content and monetisation opportunities.

Vendors need to bring that same discipline into the sales process.

The questions buyers increasingly need answered sit closer to the internal business case than the product roadmap:

- What operating problem does this solve?

- What baseline should be measured before deployment?

- Which executive functions need to be aligned?

- What governance decisions are required?

- How does this change the work?

- What adoption risks are likely?

- Where have comparable organisations stalled, and why?

These questions test whether a vendor understands the buyer’s environment, not just the technology category.

They also test whether the vendor can help reduce execution risk before the project becomes another pilot with unclear ownership and weak proof of value.

The strongest GTM teams will arrive with a view on the buyer’s operating context, likely adoption barriers, governance requirements, value baselines and executive stakeholders.

Vendor advantage now comes from reducing execution risk

AI vendors are no longer competing only against each other.

They are competing against the buyer’s internal uncertainty:

- unclear ownership, weak governance

- fragmented leadership

- poor process visibility

- immature value measurement and

- the fear of another technology investment that fails to change how work gets done.

That is why the strongest vendor narrative is not “we have better AI.”

It is “we can help you make AI work inside your organisation.”

This requires a different GTM posture.

Lead with the operating problem before the product category.

Show the organisational conditions required for value.

Bring peer evidence that explains where similar programs succeeded or stalled.

Define baselines before making ROI promises.

Treat adoption, governance and executive alignment as part of the sale.

Demonstrate AI fluency in the sales process itself.

The market is becoming harder because buyers are becoming more sophisticated, more cross-functional and less willing to carry the vendor’s translation burden.

Vendors that keep AI at the level of product comparison are pulled into feature, price and roadmap debates.

Vendors that reduce uncertainty around change earn a more valuable conversation: how the buyer can turn AI capability into measurable organisational performance.

Justina Uy

Content Marketing Manager

Justina Uy

Content Marketing Manager

Justina Uy is a data-driven content marketer that thrives on democratising elite know-how to empower Australia’s underdogs.

Skilled at translating complex ideas into a compelling story across formats and channels, she shifts seamlessly between writing long-form articles, creating viral social media posts, and producing thumb-stopping videos.

Since 2015, Justina executes her vision through a sophisticated understanding of the rapidly evolving digital and business landscape to serve entertaining and educational insights to the executive community.

Less

Join the ADAPT

Insider Community

Get the latest A/NZ market research and insights on the core trends impacting leaders.